Key Takeaways

- The agentic commerce ecosystem spans 7 layers with 90+ companies building infrastructure

- Google's UCP and OpenAI's ACP drive a protocol war, while Amazon's closed ecosystem creates a stark contrast

- VC funding concentrates in the payments and identity layer, leaving checkout execution as a notable gap

The 2026 Agentic Commerce Landscape Map at a Glance

Between late 2025 and early 2026, the agentic commerce ecosystem has grown rapidly more complex. CB Insights' market map published in November 2025 lists over 90 companies, while Rye's analysis organizes the value chain into seven distinct layers.

Understanding this market requires looking beyond "who plays where." What matters for e-commerce operators is the dynamics between layers — where money flows, where gaps remain, and where the fiercest battles for dominance are unfolding.

| Layer | Function | Key Players |

|---|---|---|

| AI Platforms | Shopping journey entry point | ChatGPT / Google AI Mode / Perplexity / Copilot / Meta AI / Amazon Rufus |

| Protocols & Standards | Common language between agents | UCP / ACP / AP2 / MCP / A2A / Visa TAP |

| Payments & Identity | Financial rails for agent transactions | Visa / Mastercard / PayPal / Stripe / Nekuda / Skyfire |

| Card Issuance | Programmable payment instruments | Lithic / Stripe Issuing / Marqeta / Highnote |

| Checkout Execution | Purchase completion on merchant sites | Rye / Induced AI / Henry Labs / CartAI |

| Merchant Enablement & Discovery | Listing & product data optimization | Shopify / commercetools / Firmly / Salsify / Feedonomics |

| Trust & Security | Fraud detection & agent authentication | Riskified / Forter / Signifyd / HUMAN Security / Kasada |

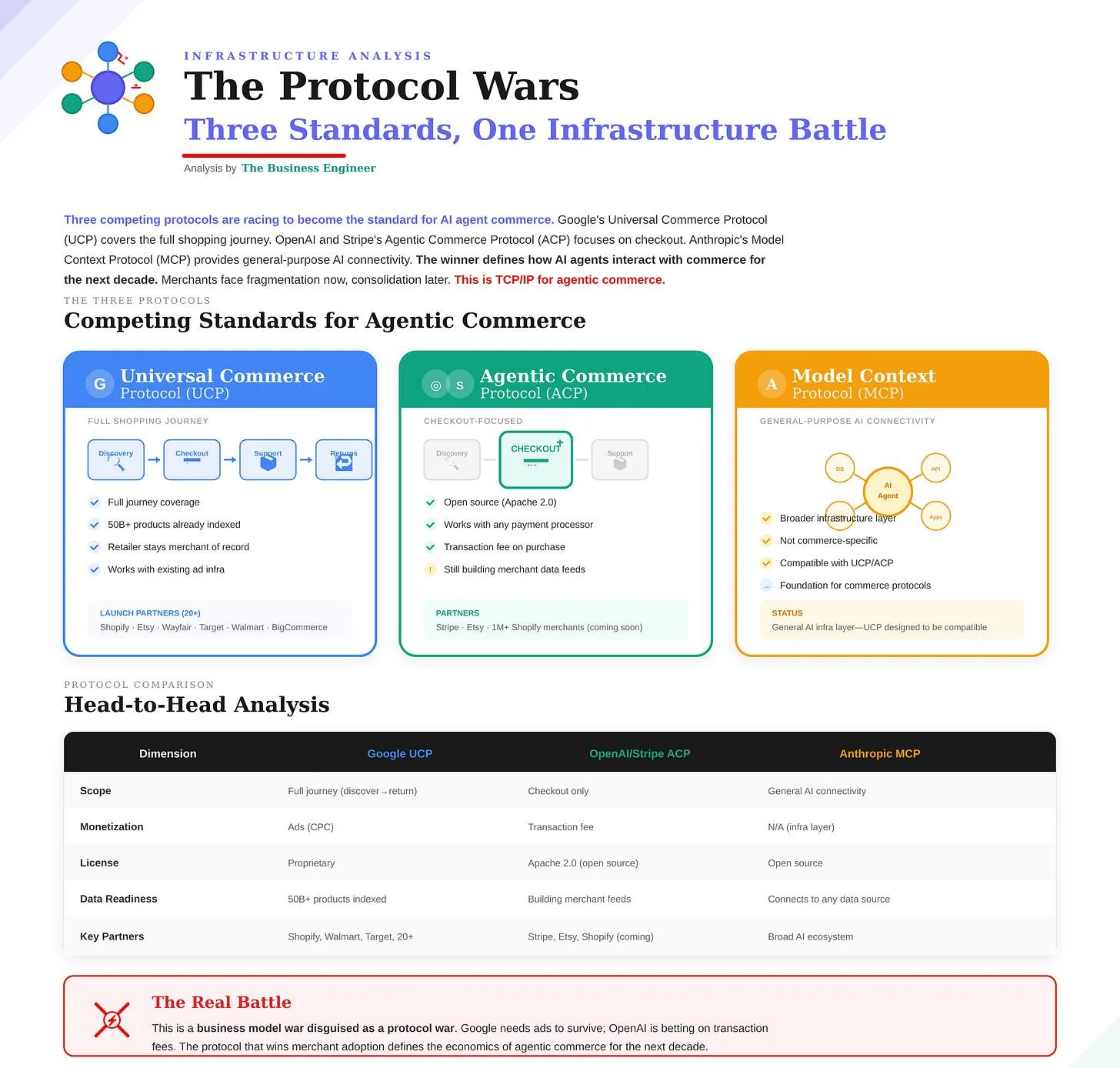

The Protocol War — A Battle for the Customer Touchpoint

The most intense competition is concentrated in Layer 2: Protocols and Standards. Whoever wins here gets to define how the entire agent-driven purchase flow works.

In January 2026, Google unveiled the Universal Commerce Protocol (UCP) at NRF 2026, and the industry landscape shifted overnight. Shopify, Walmart, Target, Wayfair, and Etsy co-developed the standard, with over 20 endorsers including Visa, Mastercard, Stripe, and American Express. UCP is a "full-stack" standard covering product discovery through post-purchase support, designed so purchases complete directly from Google's AI Mode.

OpenAI and Stripe's Agentic Commerce Protocol (ACP) takes a different approach — focused specifically on checkout and payments. Open-sourced under the Apache 2.0 license, its strength is simplicity: Stripe merchants can integrate with a single line of code. However, OpenAI paused its Instant Checkout feature in March 2026, revealing that its strategy remains a work in progress.

Will one protocol eliminate the other, like VHS versus Betamax? Analysis from MtSolutions.com suggests not. Google uses a CPC advertising model while OpenAI charges transaction fees — fundamentally different revenue structures. For merchants, supporting both protocols will likely be the pragmatic path, similar to running Google Ads and Meta Ads in parallel.

| Protocol | Led By | Coverage | Partners |

|---|---|---|---|

| UCP | Google + Shopify | Discovery → Purchase → Post-purchase | 20+ |

| ACP | OpenAI + Stripe | Checkout & Payments | 1,000+ merchants |

| AP2 | Payment Authorization | UCP-linked | |

| Visa TAP | Visa | Agent Authentication | Revolut / Barclays etc. |

| Agent Pay | Mastercard | Authenticated Payments | Santander / DBS etc. |

A third dynamic deserves attention. Amazon has joined neither UCP nor ACP, instead blocking OpenAI's crawlers and pulling 600 million products from ChatGPT search results. Only Amazon's own AI agents — Rufus AI, Alexa+, and Buy for Me — can access its catalog. This is a deliberate "closed borders" strategy.

The contrast is striking. Walmart is embracing open protocols while Amazon fortifies its walled garden. Which approach wins remains unclear, but a look at the retail giants' AI strategies shows this divergence will shape the competitive landscape for years to come.

Visa and Mastercard — The Quiet Power Behind the Protocols

While the protocol war dominates headlines, the payment networks hold more structural influence over this market's trajectory.

A Digital Commerce 360 report from early April 2026 reveals a fascinating dynamic. Despite being competitors, Visa and Mastercard face the same fundamental question in agentic commerce: how do you verify the identity of an AI agent? As Visa's Jack Forestell put it: "The agent needs an identity. You need to secure that identity, you need to validate it."

Their approaches diverge in interesting ways. Visa has deployed its Trusted Agent Protocol (TAP), aligning it with OpenAI's ACP while also endorsing Google's UCP — an "all-direction diplomacy" strategy. Partnerships with Stripe, Akamai, and AWS give it coverage across the technical stack. Mastercard, meanwhile, collaborates with OpenAI, Google, and Cloudflare on authentication standards, building its ecosystem around Agent Pay. Mastercard processed the industry's first agentic transaction in Q3 2025.

The practical implication for merchants is clear. Regardless of which AI platform wins, payments flow through Visa or Mastercard's networks. These two companies benefit from agentic commerce growth without needing to bet on a platform winner.

What VC Funding Reveals About the Real Bottlenecks

The market projections are eye-catching. Edgar, Dunn & Co estimates the agentic commerce TAM at $135 billion in 2025, growing to $1.7 trillion by 2030. McKinsey sees U.S. retail alone reaching $1 trillion in agent-mediated transactions by decade's end. Grand View Research projects $65.47 billion by 2033 at a 35.7% CAGR.

But follow the VC money and a different story emerges about where the real challenges lie.

| Company | Raised | Layer | Notable |

|---|---|---|---|

| FERMÀT | $45M Series B | Merchant Enablement | Led by VMG Partners, commerce experience optimization |

| Basis Theory | $33M Series B | Payments & ID | Tokenization infra, led by Costanoa Ventures |

| Spangle AI | $15M Series A | Infrastructure | Discovery-to-conversion unified layer |

| Limy | $10M | Merchant Enablement | Flybridge + a16z speedrun |

| Skyfire | $9.5M Seed+ | Payments & ID | a16z CSX / Coinbase Ventures |

| Firmly | $5.2M | Checkout | FJ Labs / Ark Invest / Mastercard Start Path |

| Nekuda | $5M Seed | Payments & ID | Madrona + Amex/Visa Ventures |

Funding is concentrated in the payments and identity layer. Basis Theory, Nekuda, and Skyfire alone have raised nearly $50 million. This reflects a market judgment that the infrastructure for agents to execute secure payments remains insufficient.

By contrast, the checkout execution layer has surprisingly few dedicated startups — just Rye, Induced AI, and Henry Labs. This layer remains a "white space." Even with standardized protocols, the technology for reliably completing purchases on merchant sites is still immature.

In the merchant enablement layer, FERMAT raised $45 million in its Series B and Limy secured $10 million with a16z speedrun's backing, signaling strong demand for tools that help brands optimize for AI agents. With Shopify's agentic storefronts now deployed by default across all stores, this layer's importance continues to grow.

What E-Commerce Operators Should Do Now

Based on this analysis, within the four-platform competitive landscape, merchants should focus on three actions.

First, verify which protocols your payment infrastructure supports. Stripe merchants have an easy path to ACP. Shopify merchants are getting automatic UCP support. PayPal merchants have a direct connection to Perplexity's ecosystem.

Second, invest in structured product data. Forrester predicts that five major brands will unify agentic commerce experiences in 2026, but this requires product feeds that AI can accurately interpret. Visa reports a 1,200% year-over-year increase in AI agent traffic to retail sites. Without clean data, that traffic will not convert.

Finally, watch the checkout execution layer closely. As this layer matures, AI agents will increasingly complete purchases outside your own site. Merchants who want to maintain customer relationships should explore implementing agent-compatible checkout on their own properties.

Conclusion

The 2026 agentic commerce landscape is a true chaos map — 90+ players across seven layers, competing for the infrastructure of a world where AI agents drive purchasing decisions. The protocol war, payment network positioning, and startup funding patterns all converge on a single question: who will control the rails of agent-driven commerce?

The map is being redrawn monthly. What matters is not studying the map, but deciding which layer your business will compete in.