American Express Commits to Agentic Commerce in Q1 2026 Earnings, Completing the Card Network Trio Alongside Visa and Mastercard

On its Q1 2026 earnings call, AmEx CEO Stephen Squeri said the company is only 'warming up in the bullpen' on agentic commerce. Coming after the ACE Developer Kit launch and the Hypercard acquisition, the statement completes the card network trio's full embrace of AI agent-mediated payments alongside Visa and Mastercard.

Key Takeaways

- American Express placed agentic commerce at the center of its Q1 2026 earnings narrative. CEO Stephen Squeri said the company is only "warming up in the bullpen" and "not even in the first inning" on agentic commerce.

- The April 14 ACE Developer Kit launch, the industry-first Agent Purchase Protection, and the acquisition of AI expense-management startup Hypercard Network round out AmEx's AI agent stack alongside Visa's and Mastercard's earlier moves, completing the card network trio.

- AmEx's closed-loop network and high-spend premium cardmember base form a distinct axis from Visa's "protocol-neutral on-ramp" strategy. For EC merchants, this introduces a new design question on how to route agent-led affluent-customer flows.

AmEx Declares Full AI Commitment in Q1 Earnings, Saying It Is "Not Even in the First Inning"

American Express is making AI central to its card and payments strategy, with agentic commerce initiatives discussed during Q1 2026 earnings.

www.digitaltransactions.netOn April 23, 2026, American Express released its Q1 2026 earnings and used the investor call to unambiguously stake out its position on AI and agentic commerce. According to Digital Transactions coverage, CEO Stephen Squeri told analysts that "we are warming up in the bullpen on agentic commerce. We are not even in the first inning," and signaled that more AI products will roll out later this year.

The numbers backed the rhetoric. Q1 revenue rose 11% year-over-year to $18.9 billion, card spending grew 10% (the fastest pace in three years), net income climbed 15% to $2.97 billion, and EPS was up 18% at $4.28, comfortably beating the $4.00 consensus. Premium cardmember engagement drove the growth, and Squeri described it as a "very strong start" to 2026.

The groundwork AmEx laid in the preceding weeks gave the earnings message substance. On April 14 the company unveiled the Agentic Commerce Experiences (ACE) Developer Kit, and in the same window it announced its acquisition of AI-powered expense-management startup Hypercard Network. Both moves anchor the seriousness that the earnings statement projected.

The ACE Developer Kit and an Industry-First Agent Purchase Protection

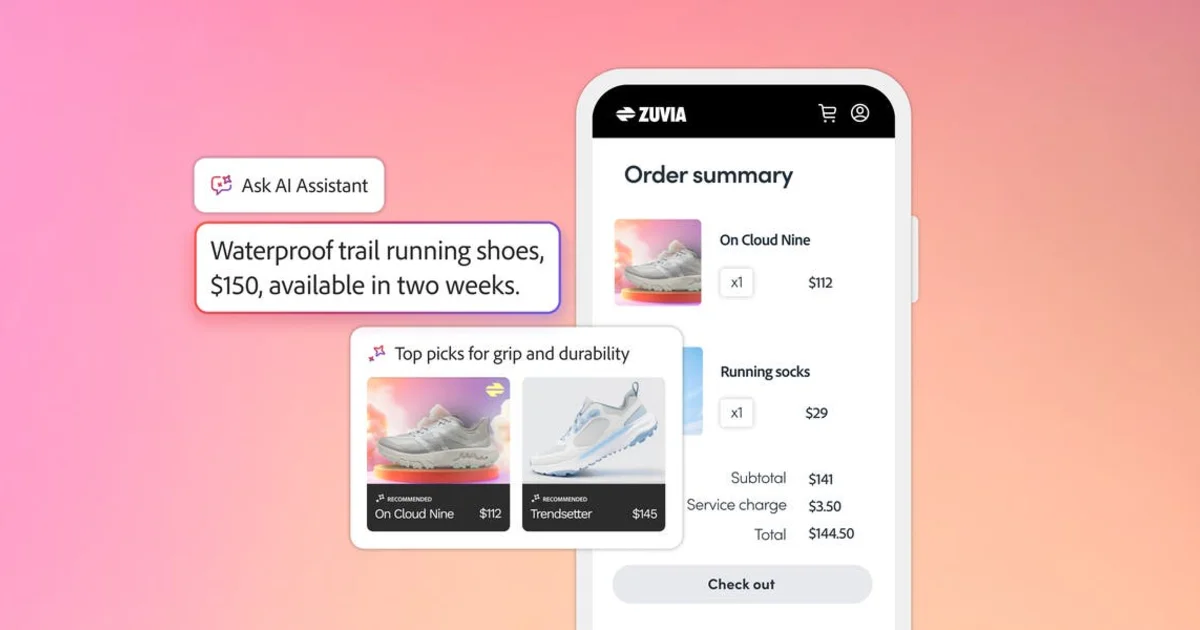

The ACE Developer Kit is the technical spec that brings American Express cards and membership value into AI agent-mediated transactions. The official press release describes five integrated services.

The first is Agent Registration, which verifies agents so that only trusted ones can transact on the AmEx network. The second, Account Enablement, lets cardmembers register their cards for agentic transactions and unlock personalized membership experiences. The third, Intent Intelligence, accurately captures purchase intent so it can feed authentication, authorization, and dispute processes. The fourth, Payment Credentials, enables verified agents to complete payments on behalf of members using tokenized credentials. The fifth, Cart Context, shares cart details before or after the transaction to tighten authorization and dispute investigation.

Equally noteworthy is Amex Agent Purchase Protection, an industry-first commitment. When a cardmember authorizes an AI agent to make a purchase and the agent sends AmEx the authenticated purchase intent, the company will protect eligible customers from charges stemming from AI agent errors. Squeri said on the call, "If our cardmembers are left holding the bag, we will back our cardmembers." This protection becomes the core brand experience of "trusting the agent" in AmEx's pitch.

The partner roster is broad. Payment providers Adyen, Fiserv, Forter, Global Payments, PayPal, and Stripe are on board from the start, as are merchants Delta, Expedia, and Hilton. The fact that the initial merchants cluster in travel and hospitality is telling: it targets the categories where AmEx's high-spend members get the most value from agentic delegation.

Comparing with Visa and Mastercard's Earlier Moves

The outlines of a three-horse race among the major card networks have hardened over the past year. The most immediate competitive reference point is Visa's Intelligent Commerce Connect, announced on April 8, 2026. According to Visa's investor announcement, it functions as an "on-ramp" for agent-initiated payments through a single integration on the Visa Acceptance Platform.

Visa's distinctive posture is being protocol- and token-vault-neutral. It supports multiple industry protocols including Trusted Agent Protocol, Machine Payments Protocol (MPP), Agentic Commerce Protocol (ACP), and Universal Commerce Protocol (UCP). By integrating non-Visa network APIs as well, it can process payments on non-Visa cards too. Pilot partners include Aldar, AWS, Diddo, Highnote, Mesh, Payabli, and Sumvin, with broader rollout planned this year.

Mastercard was first out of the gate with Agent Pay in April 2025. Through 2026 it has spread the footprint laterally with Australia's first fully authenticated agentic transactions, expansion into ASEAN, participation in Google's Universal Commerce Protocol and OpenAI's Agentic Commerce Protocol, and a "Virtual C-Suite" offering for small businesses. The Mastercard Agent Suite for operational integration is scheduled for Q2 2026.

| Card Network | Key Products / Initiatives | Announcement Timing | Differentiation Axis |

|---|---|---|---|

| American Express | ACE Developer Kit + Agent Purchase Protection, Hypercard acquisition | April 14-23, 2026 | Closed-loop network, purchase protection, premium cardmember base |

| Visa | Intelligent Commerce Connect (Visa Acceptance Platform integration) | April 8, 2026 | Protocol- and token-neutral 'on ramp', multi-network support |

| Mastercard | Agent Pay + Agent Suite (Q2 2026 availability) | April 2025 - 2026 | Participation in industry standards such as Universal Commerce Protocol, Virtual C-Suite for SMBs |

Lined up side by side, the strategic differences sharpen. Visa aims to be the platform that "accepts any agent and any protocol." Mastercard broadens through industry-standard participation and an SMB ecosystem. AmEx differentiates via a trust layer built on closed-loop and purchase protection. The three paths compete, but each mines the same agentic commerce market from a different angle.

AmEx's Differentiation: Closed-Loop and Depth of KYC Data

It is worth spelling out where AmEx structurally differs from the other two. First comes the closed-loop network. Visa and Mastercard slot the network between separate issuers and acquirers, an "open loop" model. AmEx owns issuing, acquiring, and the network in one stack. That means cardmember purchase intent and merchant cart data can be reconciled inside the same operator.

The biggest risk in agentic commerce is who guarantees that "agent-declared intent" matches "the transaction that actually occurred." Squeri said on the call that "agents need to declare purchase intent and match that with what is actually purchased. We can get that data. We don't even have that in the physical world." A closed-loop architecture consolidates that reconciliation in a single data plane, which could become a structural advantage over open-loop networks.

The other lever is depth of KYC and fraud data. As an issuer, AmEx has accumulated years of per-member spending history, income tiers, and loyalty-program engagement. In the agent era, risk scoring that asks "does this purchase match the member's pattern?" and "has the agent strayed from reasonable judgment?" sits upstream of each transaction. AmEx can bring the highest-quality training data to that layer.

There is also the premium cardmember base as a business property. AmEx members skew toward higher average ticket sizes and categories such as travel, dining, and entertainment, which are precisely the areas where "delegating to an agent" delivers the most user value. It is not a coincidence that the initial ACE merchants are Delta, Expedia, and Hilton. The strategy is to capture affluent-customer agentic use cases first.

NFL Partnership and the Subtext of the Corporate Segment

Two other threads surfaced on the call. The first is the official NFL payments partnership that begins with the 2026 season. Squeri framed the marketing payoff directly. On the agentic commerce axis, the touchpoints will be ticket purchases, in-stadium payments, and personalized fan-merchandise recommendations — event-linked agent use cases.

The second is a plan to introduce new or enhanced commercial cards with stronger spend and cash-flow management. The acquired Hypercard Network's expense-management AI is likely to feed into this. B2B corporate spend is a traditional AmEx profit pool, and the use case of employee-side agents paying expenses on behalf of companies may reach production use ahead of consumer agentic payments. A pattern where an employee's agent books travel or orders supplies, with AmEx providing purchase protection, slots directly into B2B SaaS payment workflows.

What EC Merchants Should Watch

From the vantage point of EC merchants and D2C brands, three implications deserve attention.

First, operators of high-ticket categories should evaluate AmEx's agent route now. Amex Agent Purchase Protection lowers the psychological hurdle of agent-led purchases, which means high-priced items may see conversion rates via agentic checkout that beat the other networks. In travel, luxury, consumer electronics, and B2B supplies, connecting to ACE alongside Visa and Mastercard helps prevent leakage of premium customers.

Second, architect for protocol diversity. Agentic Commerce Protocol, Machine Payments Protocol, Universal Commerce Protocol, Trusted Agent Protocol — industry protocols are converging on a multi-standard coexistence model. Visa offers a neutral on-ramp, while AmEx pushes its proprietary ACE spec. Merchants should ask payment gateways and orchestration vendors which protocols they will support.

Third, treat intent signals as a data asset. Both ACE's Intent Intelligence and Visa's Intelligent Commerce Connect put weight on the "intent information" an agent sends at checkout. Whether a merchant can deliver structured cart data and product catalogs determines authorization success and dispute resilience. The investment that once went into SEO and paid listings for human clicks needs to rotate gradually toward catalog readiness that lets agents discover and select.

Conclusion

AmEx's Q1 declaration is not a standalone strategy announcement but a signal of a market-structure shift: all three major card networks are now fully committed to agentic commerce. Visa provides a protocol-neutral on-ramp with Intelligent Commerce Connect (April 8). AmEx brings a trust layer with the ACE Developer Kit and Agent Purchase Protection (April 14). Mastercard already shipped Agent Pay and has Agent Suite coming in Q2 2026.

For EC merchants, the right framing is not "which network do we pick" but a three-layer response: protocol standardization, agent-readable catalogs, and intent-data handoffs. Whether AmEx's purchase protection wins in the high-ticket segment, whether Visa's multi-network strategy becomes the universal on-ramp, and whether Mastercard's ecosystem-width strategy dominates among SMBs — the market's answers will begin to emerge from late 2026 into 2027. Squeri's "not even in the first inning" is less optimistic marketing and more an accurate read on how long this game will run.