Key Takeaways

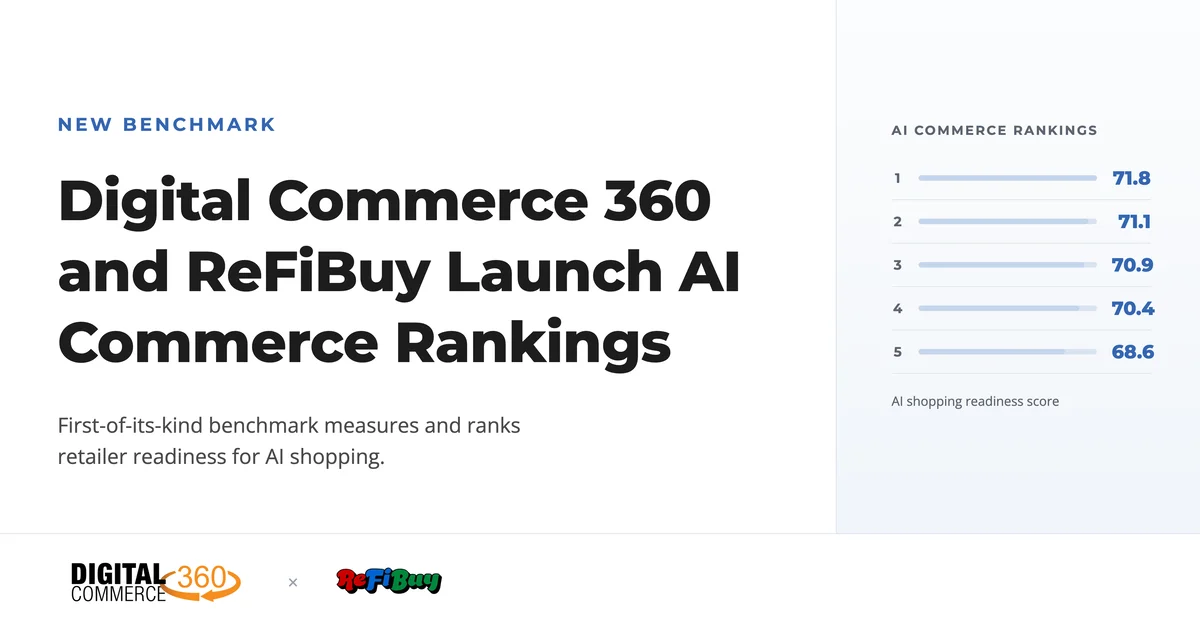

- Digital Commerce 360 and ReFiBuy have launched the AI Commerce Rankings, a quarterly benchmark that scores the Top 1000 U.S. online retailers from 0 to 100 on their readiness for AI shopping

- The first edition is led by Online Labels (71.8), ranked No. 814 by online sales. With an average score of just 41.9 across all 1,000 retailers, the data confirms that sales scale and AI readiness barely correlate

- More than 80% of AI-referred retail traffic comes from ChatGPT. For e-commerce operators, the rankings point to concrete actions: catalog data hygiene, UCP/ACP support, and diversifying AI traffic sources

A Second Scoreboard Next to the Sales Rankings

Digital Commerce 360 and ReFiBuy have introduced the AI Commerce Rankings, a quarterly benchmark that scores Top 1,000 retailers on AI shopping readiness.

www.retailtouchpoints.comFor more than two decades, Digital Commerce 360's Top 1000 has served as the definitive winners list of U.S. e-commerce. In July 2026, an entirely different yardstick appeared alongside it. The AI Commerce Rankings, co-developed with commerce intelligence company ReFiBuy, score every retailer in the Top 1000 from 0 to 100 on their readiness for AI shopping agents, recalculated every quarter. Where the traditional ranking measures estimated online sales — past performance — the new index measures something forward-looking: whether AI shopping agents can read, interpret, and recommend a retailer's product catalog.

ReFiBuy is led by Scot Wingo, best known as the founder of e-commerce software giant ChannelAdvisor. He launched ReFiBuy in 2025 with fellow ChannelAdvisor alumni, building a business around evaluating and optimizing product catalogs for AI agents. In this partnership, ReFiBuy co-developed the methodology and produced the underlying data and scoring, while Digital Commerce 360 contributed the retailer universe and its editorial and research framework.

Estimated online sales show who won the last era of ecommerce. The AI Commerce Rankings show who is positioned to win the next one.Source: Scot Wingo (CEO, ReFiBuy)

The timing is no accident. According to Adobe data cited in the launch announcement, AI-source traffic to U.S. retail sites grew 693% year over year during the 2025 holiday season and remained elevated in 2026, up 393% year over year in the first quarter. By ReFiBuy's count, 87.1% of the Top 1000 already receive measurable AI traffic, and the first edition covers roughly 109 million AI-source visits. AI-driven customer acquisition is no longer a forecast — it is a measurable reality.

The Four Signals Behind the Score

Each retailer's score is built from four signals that reflect what AI shopping agents actually observe when they reach a catalog.

| Signal | What it measures | Key focus |

|---|---|---|

| Bot friendliness | Whether AI agents can access, read, and transact with the catalog | Includes support for agentic commerce protocols such as UCP and ACP |

| AI source traffic | Volume of traffic from answer engines | How much AI-referred traffic the retailer already receives from ChatGPT, Gemini, and others |

| Diversity of AI sources | How dispersed AI traffic sources are | Whether traffic spans multiple engines or concentrates on a single one |

| 90-day momentum | Growth or decline of AI traffic over the trailing 90 days | Evaluates the quarterly trend rather than a point-in-time snapshot |

The heaviest theme here is bot friendliness. It goes well beyond whether a retailer blocks crawlers: the signal evaluates support for agentic commerce protocols such as Google's Universal Commerce Protocol (UCP) and the OpenAI and Stripe-backed Agentic Commerce Protocol (ACP). The question is not only whether agents can read products, but whether they can buy them. The 90-day momentum signal, meanwhile, tracks the trailing quarter's trend rather than a single snapshot, which deliberately leaves room for late movers to catch up.

One design caveat matters a great deal. A low score does not mean a retailer has no AI strategy. Every input is limited to what agents can observe from the outside, so internal preparation that agents cannot yet see simply does not register. Put another way, the index is a mirror of how retailers appear to AI agents — fundamentally different in nature from a self-reported survey. Scores are recalculated quarterly, and the methodology itself is re-evaluated on the same cadence, with each edition documenting any algorithm changes.

A First Edition Won by the No. 814 Retailer

The first edition's leaderboard defies the conventional pecking order of e-commerce. The top spot went to Online Labels, a label and sticker printing specialist, with a score of 71.8 — a company that ranks No. 814 by online sales. Watch brand Nixon (No. 722 by sales) follows at 71.1, luxury handbag reseller Fashionphile (No. 826) takes third at 70.9, and Everlane (70.4, No. 264) and Brooklinen (68.6, No. 331) round out the top five. Not a single sales heavyweight appears among them.

The aggregate numbers are even more sobering. The average score across all 1,000 retailers is 41.9 and the median 44.1, with only 20 retailers scoring above 60. The highest score is 71.8, meaning virtually no retailer reaches what could be called a passing grade on a 100-point scale. According to the original article, one top-10 retailer by online sales ranks below No. 550 on AI readiness.

The category breakdown is just as revealing. Office supplies leads all 15 categories with an average of 47.4, small in scale but pairing the highest average score with the highest AI traffic penetration in the index. Jewelry ranks second at 45.0 with the most diversified answer-engine visibility of any category, and hardware and home improvement comes third at 44.8, driven by niche specialists rather than household names. At the other end, food and beverage — the largest arena of consumer shopping overall — sits last at 37.2, while mass merchants average 179 places lower on AI readiness than on sales rank, the widest gap of any category. Automotive is the outlier: not one retailer in the category has verified UCP support, yet its AI traffic penetration runs above the index average, which is why ReFiBuy calls it the most open field in the rankings.

There are structural reasons for the inversion between scale and readiness. Large retailers carry catalogs with millions of SKUs, complex legacy systems, and security postures that often block agent access outright. The DTC brands and niche specialists at the top, by contrast, manage product data centrally with simpler catalog structures. As Wingo put it at launch, "Agents want to know every detail about every product." What is being tested is not capital, but how well-groomed the data is.

The Reality of ChatGPT's 80%-Plus Share

The first edition surfaced another hard fact: an extreme concentration of traffic sources. ChatGPT accounts for more than 80% of AI-referred retail traffic. Source diversity earns its place as a standalone scored signal precisely because this concentration represents genuine platform risk for retailers.

Depending on a single engine recreates the Google-dependency dynamic of the search era, but at a far faster pace of change. Google Gemini, Alexa for Shopping, and other emerging answer engines are already influencing product discovery, and the share breakdown will certainly shift. Rather than taking comfort in growing ChatGPT referrals, the dividing line in this index is whether a retailer is equally visible across multiple engines.

What E-Commerce Operators Should Take Away

The arrival of this index marks the start of an era in which "how you appear to AI agents" is contested on a public scoreboard alongside sales rankings. With quarterly updates and industry media coverage, AI readiness is being promoted from an internal to-do list to a management-level metric.

The playbook maps directly onto the four signals. Start with an audit of how your site appears to agents: whether robots.txt or bot-management tools are blocking AI agents indiscriminately, and whether product data is readable in structured form. Next comes protocol support — by ReFiBuy's count, only 26% of the Top 1000 have verified UCP status, so support itself is still a differentiator. Then come source diversification and managing momentum in 90-day increments. The existence of the momentum signal means a low rank today can be moved within a quarter. Indeed, an average of 41.9 in the first edition is proof of how immature this competition still is — immature enough that early movers, even niche companies, can take the top spot.

Conclusion

The AI Commerce Rankings are the first attempt to make the progress of agentic commerce visible not through individual company announcements but through industry-wide, recurring measurement. The first edition revealed the divergence between sales scale and AI readiness, the concentration of AI traffic in ChatGPT, and the competitive white space left by only 20 retailers scoring above 60. Because scores refresh quarterly, the next edition will spotlight whether the majors fight back and how protocol adoption rates change. Will the sales-ranking incumbents keep sliding, or will their preparations finally become observable to agents? As a metric that tracks the quiet setup phase before agent-driven purchasing goes mainstream, it deserves ongoing attention.