Klarna's CEO on the Fight for 'Top of Wallet' When AI Does Your Shopping

Klarna CEO Sebastian Siemiatkowski told Semafor's podcast that brand preference still wins even when AI agents shop for you, reframing the 'top of wallet' fight. We unpack preference, bank plans, and the DoorDash BNPL debate for merchants and payment teams.

Key Takeaways

- Klarna's CEO argues brand preference survives even when AI does the shopping, moving the decades-old "top of wallet" fight into a new arena

- Bots are hard to advertise to or reward, so pre-built preference becomes the lifeline for payment players when agents pick the method

- Klarna is embedding itself in agent journeys via a ChatGPT app and Google's protocols, planting flags to stay the default payment choice

Preference in a World Where Bots Shop

CEO Sebastian Siemiatkowski thinks there's still a place for brand loyalty and perks in a bot shopping world.

www.semafor.comOn June 9, 2026, Klarna CEO Sebastian Siemiatkowski appeared on Semafor's podcast "Compound Interest." The topic was how to fight for "top of wallet" in a world where AI agents do the shopping. This seat at the front of the wallet, contested for decades by credit card companies, is taking on a new shape in the AI era.

The rise of agentic commerce has handed e-commerce players a fresh anxiety. When swarms of bots fill shopping lists, the ads and rewards aimed at humans no longer land. Agents insert a layer of abstraction between the shopper and the choice of what to buy and how to pay. Siemiatkowski believes brand preference holds up anyway.

If you have preference, it doesn't matter that much how many buttons are in the checkout or what happens in the world with new things, because you have that brand affinity.Source: Sebastian Siemiatkowski

How "Top of Wallet" Changes Meaning

Top of wallet refers to the position of being chosen first as a payment method. The phrase comes from the card you reach for first when you open your wallet. Card issuers have competed for that spot with cashback and sign-up perks for years.

Once AI agents handle payment, however, the one opening the wallet is no longer human. Agents are unmoved by perks and slow to respond to ads. Siemiatkowski's point is that in exactly this environment, brand preference built up in advance starts to matter. Through the instructions and settings a user gives an agent, there is still room for someone to say "pay with Klarna."

He also touched on Klarna's competitive standing, expressing confidence that it wins when BNPL providers sit side by side.

When Klarna is side by side with some of the other buy-now-pay-later providers, we win on preference.Source: Sebastian Siemiatkowski

The Moves to Secure Agent Exposure

Talking about preference alone does not get you into the bot's shopping cart. Through 2026, Klarna has moved quickly to embed itself directly in the agent's path.

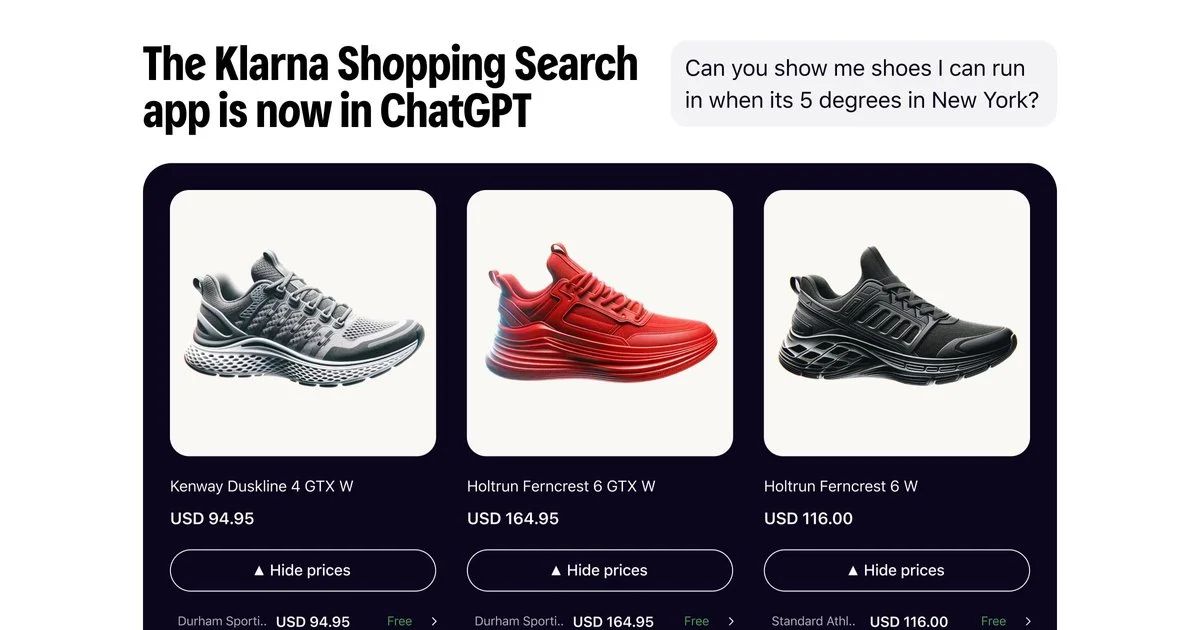

On May 20, 2026, Klarna launched a shopping search app running inside ChatGPT. Without leaving ChatGPT, users can search products, compare prices, check availability, and view offers across multiple retailers. The app runs on Klarna's Product Search MCP server, spanning 13 markets with more than 100 million products and 400 million merchant listings. Through MCP (Model Context Protocol), AI agents access product catalogs, pricing, and stock in real time.

On the payment side, Klarna brings its BNPL product into agentic commerce via Stripe's Shared Payment Tokens. In its work with Google, it offers BNPL in AI Mode alongside Affirm and supports Google's Universal Commerce Protocol (UCP) and Agent Payments Protocol (AP2). The goal is to close the interoperability gap between conversational agents and backend payments by riding industry standards. Owning both the discovery entrance and the payment exit is the groundwork for winning top of wallet in the agent era.

The Reality of Banking and AI Customer Service

Behind the top-of-wallet fight, the shape of Klarna's business is shifting too. The company listed on the New York Stock Exchange on September 10, 2025, pricing at $40 per share and raising roughly $1.37 billion. As a public company, expanding from payments into banking has become a real option.

Siemiatkowski signaled direction on a US bank charter as well. In Europe, Klarna already operates as a bank, holding around $12.3 billion in deposits across 11 markets. In the US, it offers high-yield savings through WebBank and is not itself a bank. He said it would make sense to move toward becoming a bank in the US over time.

Directionally speaking, it would make sense for us to do so over time in the US.Source: Sebastian Siemiatkowski

Klarna's AI experience carries its own lesson. In February 2024, the company deployed an AI assistant built on OpenAI's models and said it handled the work of roughly 700 customer service agents. But satisfaction dropped on complex inquiries, and through early 2026 the company partially reversed course. Siemiatkowski himself admitted that an overemphasis on efficiency and cost lowered quality. AI stays on the front line for high-volume, routine cases, while humans return for complex, high-value work. That boundary became the practical settling point for dividing labor between AI and people.

What the DoorDash Installment Debate Reveals

The symbol of Klarna's BNPL reaching into everyday life was its DoorDash partnership. Announced in March 2025, it lets food delivery customers pay in full, in four installments, or push payment to a later date such as payday. Siemiatkowski touched on the deal during the podcast.

Still, the idea of paying for takeout in installments drew criticism. On social media, the concern aimed less at the companies than at an economy where people feel they must split a meal into payments. The fact that US household debt topped $18 trillion at the end of last year sits in the background of that debate.

From a payment team's perspective, this is more than a flare-up. Where BNPL should reach into the purchase journey ties directly to brand trust. In a world where agents handle payment, part of that judgment gets delegated to algorithms. That is precisely why a design philosophy about which payment is allowed in which moment will shape whether you can win top of wallet.

What Merchants and Payment Teams Should Read Into This

What this interview puts in front of merchants and payment teams is a reality: the path to reaching customers now runs through bots. Banners and points aimed at human eyes may be bypassed entirely by an agent.

The response splits in two directions. One is making sure your brand sits at the "entrance" of the product data and payment options agents reference. Support for MCP servers and standards like UCP and AP2 pays off here. The other is building brand preference while a human is still in the loop. The initial settings and instructions a user gives an agent ultimately depend on preference formed through past experience.

Even when AI picks the payment method, the criteria for that choice are first shaped by human trust. Klarna's strategy reads as an attempt to make the intangible asset of preference concrete through exposure and standards support built for the agent era.

Conclusion

The core of Siemiatkowski's argument is that brand preference does not vanish even when AI shops for you. Bots are hard to reach with ads and perks, yet the preference a user has accumulated still flows into the agent's choice. On that read, Klarna is securing exposure through its ChatGPT app and Google protocol support, planting flags to remain the first payment choice.

What to watch next is who controls the "default settings" agents use when picking a payment method. If platforms like ChatGPT or Google hold a default payment, control of the entrance may outweigh accumulated preference in some scenarios. Whether the main battlefield of top of wallet shifts from the consumer's wallet to the agent's default settings is the dividing line for reading the payment competition in agentic commerce.