Why Value-Added Services Are Fueling Visa's Growth: Inside Its Agentic Commerce and AI Fintech Push

Visa is rapidly partnering with AI fintechs like Alchemy and Nuvion to grow value-added services (VAS) — a non-payment revenue metric investors watch closely — through agentic commerce and stablecoins.

Key Takeaways

- In a single week, Visa announced back-to-back partnerships with AI fintechs including Alchemy and Nuvion, rapidly building the infrastructure for AI-agent payments

- The goal is to grow "value-added services" (VAS) revenue beyond card payment fees. VAS is the metric investors watch most closely, and it grew 27% year-over-year last quarter

- For commerce and booking businesses, Visa's moves signal that AI-agent purchasing is shifting from the "experimentation" phase to real-world use

Visa Lines Up AI Fintech Partnerships to Fuel Value-Added Services

Visa's recent partnerships attempt to build demand for new forms of artificial intelligence while feeding 'value added' revenue — a metric that payment investors watch closely.

www.americanbanker.comIn June 2026, Visa announced a rapid-fire series of AI fintech partnerships within the span of a single week. They included AI developer Alchemy, AI-powered cross-border payments platform Nuvion, and MiniPay, the stablecoin wallet owned by Opera. These moves may look scattered, but they share a single underlying objective.

That objective is to build out a new revenue source that does not depend on payment fees at the point of sale. According to American Banker's reporting, these partnerships are part of a strategy to strengthen "value-added services" (VAS) as card payment fees come under pressure from regulation and fintechs.

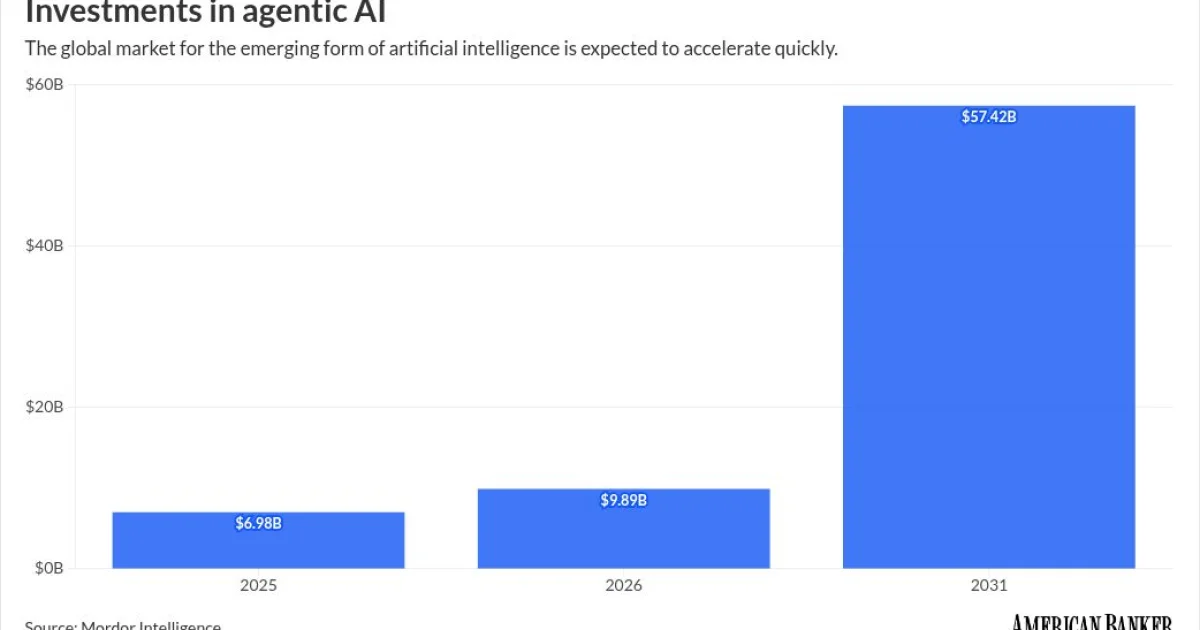

Agentic commerce — where AI agents make purchases and bookings on behalf of humans — has not yet reached mainstream usage. Visa is investing early to capture the demand it expects to arrive, building it on top of its own infrastructure.

What Exactly Are "Value-Added Services" (VAS)?

To read Visa's earnings, you need to understand VAS. VAS refers to non-payment revenue generated by the services Visa provides on top of its network, distinct from the per-transaction fees (such as interchange) it earns on card payments. Concretely, it includes fraud detection, tokenization, consulting, data analytics, and — as in this case — infrastructure for AI agents.

Why do investors watch this number so closely? Because payment fees themselves face continuous pressure from both regulators and fintechs. Conventional volume-linked revenue has a more visible growth ceiling, while VAS is valued as the "upside" — a layer where Visa can keep stacking new services on top of its vast payments network.

The category is indeed growing fast. In Visa's fiscal Q2 2026 results, VAS revenue rose 27% year-over-year to $3.3 billion, reaching roughly 30% of total net revenue. Both Visa and Mastercard reported more than 20% year-over-year VAS growth last quarter, and analysts at research firm TD Cowen described the two as "pairing durable core payments growth with meaningful VAS contribution."

Analysts at William Blair likewise framed this trend as a "tailwind" for Visa, noting that securing agentic transactions and supporting open banking underpin an outlook for steady yield accretion. VAS is not a side income stream — it sits at the center of Visa's growth story.

What the AI-Agent-Only "AgentCard" Reveals

The most symbolic of these partnerships is the collaboration with AI developer Alchemy. Alchemy integrated AgentCard, its identity and payment platform for AI agents, into Visa Intelligent Commerce, Visa's agentic commerce portal.

The problem AgentCard tries to solve is clear. Alchemy CEO Nikil Viswanathan points to the fact that existing financial infrastructure was designed for humans.

Banks are designed for humans. They can proactively go to a website, access the bank, and get a card. Now we're seeing this wave of AI agents that can't easily use the infrastructure that was built for humans.Source: Nikil Viswanathan (CEO, Alchemy)

Agents cannot pass know-your-customer (KYC) and anti-money-laundering checks as-is. So AgentCard issues a Visa payment token, a dedicated email address, a phone number, and a crypto wallet to an AI agent through a single API. This lets agents built on models from OpenAI, Anthropic, or others book a vacation, order food, or renew a subscription on a person's behalf — without the user ever touching a checkout screen.

The early numbers are worth noting. According to CoinDesk and Alchemy's press release, this digital card for AI agents drew 78,000 sign-ups in its first 48 hours. That is a tiny fraction of the billions of credit cards in circulation, but as Viswanathan put it, "there aren't many people who have an AI agent yet, so there is demand."

Expanding Into Cross-Border Transfers and Stablecoins

If AgentCard is the entry point for consumer-facing agent payments, the other two partnerships strengthen the transfer and settlement rails behind it.

Visa integrated Nuvion into its Visa Direct real-time transfer system. By combining Nuvion's cross-border payments AI, businesses can automatically facilitate transfers through multiple options — cards, multicurrency accounts, foreign exchange, and stablecoin settlement rails. Once again, the keyword is automation, envisioning a world where AI chooses the optimal payment route.

In a separate move less directly tied to AI, Visa partnered with MiniPay — the stablecoin wallet owned by Norwegian fintech Opera — to launch a card that lets users spend stablecoin balances at more than 175 million merchants. Jørgen Arnesen, Opera's EVP of mobile, said MiniPay "was built to make stablecoins useful in everyday life, not just to hold or send, but to spend."

Stablecoins are becoming a strategic pillar for Visa. In its latest earnings, stablecoin-linked card program volume nearly tripled year-over-year, reaching a roughly $7 billion annualized settlement run rate. Visa is cultivating two fields at once — AI agents and digital assets — both areas with high interest but limited usage so far.

The Visa-Mastercard Competitive Picture

This is not Visa acting alone. Behind it lies a competition with rival Mastercard to make agentic commerce the next growth engine.

In 2025, Visa launched Trusted Agent Protocol, a framework to authenticate trusted AI agents and distinguish them from rogue ones. Its partners include payments and commerce heavyweights such as Adyen, Ant, Checkout.com, Coinbase, Microsoft, Shopify, Stripe, and Worldpay. Major AI platforms including OpenAI, Anthropic, and Perplexity have also joined, as Visa moves to own the industry standard for agent authentication.

Mastercard, for its part, pairs Merchant Cloud — which lets merchants conduct agentic payments — with Mastercard Agent Pay, and offers fraud-monitoring tools to spot fake merchants. The two networks' playbooks are strikingly similar: defend core payments growth while positioning agentic commerce and stablecoins as complementary infrastructure layers that expand the long-term addressable market. That shared view is the force moving the entire industry right now.

Implications for Commerce and Booking Businesses

So what does all of this mean for businesses that sell goods and services?

The most important takeaway is that AI-agent purchasing is shifting from "experiment" to "real-world use." Rubail Birwadker, Visa's global head of growth products and partnerships, said what has changed over the past year is the "pace and depth" of these partnerships, with the technology advancing from experimentation to practical use. AgentCard drawing more than 70,000 sign-ups in 48 hours shows the demand is real.

The issues commerce and booking businesses should prepare for can be summarized as follows.

| Issue | Traditional (human buying) | What the agent era requires |

|---|---|---|

| Customer identification | Verify identity via login ID or card details | Authenticate legitimate AI agents and separate them from rogue ones |

| Checkout | Humans operate a screen to pay | Support purchases completed via API without a screen |

| Fraud and risk | Detection assumes human behavior patterns | Handle agent-specific transaction patterns and tokens |

| Product and inventory data | Human-friendly page display | Structured data and APIs that agents can access |

As card networks move to own the standards for agent authentication and payment tokens, merchants will need to rethink their checkout, fraud controls, and inventory and pricing displays on the assumption that "non-human agents are purchasing as legitimate customers." What Visa is building is the foundation that lets those purchases settle safely. In a world where agents pick the products, structured product data and API-accessible inventory will become the conditions for being chosen.

Conclusion

Read as isolated headlines, Visa's partnerships are hard to interpret. Connected, they trace a single strategic line: grow VAS revenue that does not rely on payment fees, across two new frontiers — agentic commerce and stablecoins.

Usage is only just beginning, and consumers using AI agents remain few. Even so, the fact that card networks are rushing to build authentication protocols and agent-only cards reflects a decision to secure the foundation before demand takes off. The next things to watch are how much sign-ups for schemes like AgentCard convert into actual transaction volume, and how far VAS growth rates climb in the coming quarters.