Key Takeaways

- With Universal Cart at the center, Google has made its strategy explicit: enclose the entire shopper journey from discovery to purchase inside Gemini, intensifying the battle for agentic commerce.

- The real contest is not Google versus OpenAI but a fight for control between "horizontal agents" that move across their own ecosystems and "vertical agents" that own a specific commerce domain.

- Merchants should design for distribution across multiple AI touchpoints rather than optimizing for a single platform, and build transparency on the assumption that shoppers remain distrustful.

What Universal Cart Reveals About Google's Real Aim

Google's aim to own the entire shopper journey is heating up the agentic commerce battle against Amazon's Alexa and rivals like TikTok Shop.

digiday.comThe Universal Cart that Google unveiled last week is an "intelligent shopping cart" that works across retailers and services. A shopper can add items to the same cart whether they are in Search, Gemini, YouTube, or Gmail. The mechanics themselves are something we have already covered in our explainer on the Universal Commerce Protocol (UCP). What deserves attention this time is not the feature set but the reach of the strategy behind it.

A commerce executive who spoke to Digiday on condition of anonymity described the announcement as "not just about agentic commerce, but a new commerce experience that will show up on a lot of Google's most used surfaces — YouTube, Search, Ads, and Gemini." In other words, what Google is drawing up is not a specific feature but a structure that completes the entire shopper journey inside its own surfaces.

Ashish Gupta, Google's VP and GM of merchant shopping, told a roundtable ahead of Google Marketing Live, "We are not a retailer, we are not a marketplace, and that approach continues to guide us in this agentic era." Google intends to remain the "matchmaker" between shoppers and brands. Molly Schonthal, managing director of agentic commerce at VML, framed the roadmap as "the beginning of a broader restructuring of commerce around AI agents and assistant-driven decisioning."

This "intermediary" stance extends the revenue structure Google built with search advertising. Rather than handling retail itself, Google treats its vast troves of discovery and purchase-intent data as assets and aims to stay positioned between shoppers and brands. That is precisely why its rivals emerge as threats to the intermediary position itself.

Horizontal Agents vs. Vertical Agents

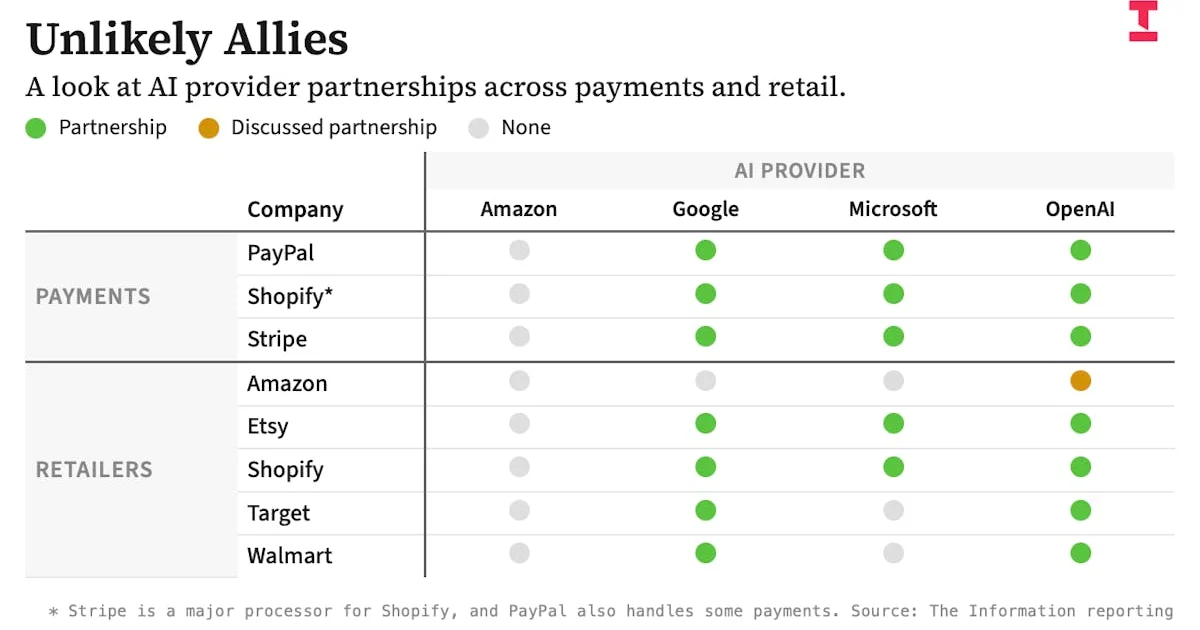

Viewing the agentic commerce contest as "Google versus OpenAI" misses the point. The anonymous executive offered a sharper frame: this is a fight between two camps — "horizontal agents" such as Google, OpenAI, and Anthropic that operate across their own ecosystems, and "vertical agents" such as Amazon and Walmart that operate within a specific commerce domain.

The strength of horizontal agents lies in owning touchpoints across daily life — not just purchases, but search, video, and email. Gemini can enter at the vague "what should I buy" stage before a shopper has even started searching. When Tinuiti's VP of commerce media Elizabeth Marsten said the thing Google did "more than anything else was getting us comfortable with the conversation with essentially a computer — to get to answers faster," she was pointing to the breadth of that entry point.

Vertical agents, by contrast, compete on the certainty of completing the purchase. This month Amazon integrated its LLM-powered assistant Alexa+ into its shopping experience and replaced its shopping-specific assistant Rufus with Alexa for Shopping. An agent that used to live inside a chat window now sits behind every search box Amazon owns, instantly connecting it to roughly 300 million U.S. shoppers and more than 600 million Alexa endpoints. With "Buy for Me," it can even execute purchases on external sites — a vertical agent reaching into horizontal territory.

The clearest way to put it: horizontal agents are trying to own the "entrance to the decision," while vertical agents are trying to own the "exit of the transaction." Even if Google captures the entrance through Search and Gemini, the shopper journey will cross camps midway if Amazon holds the final checkout and fulfillment. Universal Cart's design — running everything from search to checkout via Google Pay — is precisely a move to keep that exit out of Amazon's hands.

How TikTok Shop and Meta Changed the Temperature

Part of what pushed Google this far is pressure from social commerce. Phil Case, president and chief client officer at the performance agency Max Connect Digital, reads the UCP updates this way: Google is "seeing the massive volume of transactions and shopping coming out of TikTok Shop and Meta, and saying, 'We want a piece of that.'"

The numbers are not something to brush aside. TikTok Shop is projected to reach $23.4 billion in U.S. ecommerce sales in 2026, a 48% increase. The Wall Street Journal, citing ecommerce data provider Charm.io, reported it has already driven $4.9 billion in U.S. sales. TikTok Shop's edge is the frictionless path from discovery to purchase: creators demonstrate products and viewers tap a tag and buy without leaving the entertainment flow.

Meta is not standing still either. In March 2026, Bloomberg reported that Meta is testing a shopping research feature in its AI chatbot to rival Gemini and ChatGPT. ChatGPT's Instant Checkout once attempted web-wide payments too, but its merchant fee model stalled adoption and forced a retreat. With each player entering on different strengths and different revenue models, agentic commerce has settled into a structure where no single winner is decided and the scramble for touchpoints continues.

For merchants, the key consequence of this fragmentation is that it removes the option of "just bet on one company." Discovery happens on Google or TikTok, comparison happens in Gemini or ChatGPT, and checkout happens on Amazon or a brand's own site. The shopper journey now runs across multiple camps.

| Dimension | Google (Gemini) | Amazon (Alexa for Shopping) | TikTok Shop |

|---|---|---|---|

| Agent type | Horizontal (cross-surface) | Vertical (own domain) | Vertical (content-led) |

| Primary touchpoints | Search, YouTube, Gmail, Gemini | Amazon search, Alexa devices | Short-form video, live streams |

| Commerce protocol | UCP (Universal Commerce Protocol) | Proprietary ecosystem + Buy for Me | Closed in-house platform |

| Merchant's position | Supplier behind a matchmaker | Marketplace seller | Creator-linked seller |

| Core strength | Discovery and purchase-intent data | Conversion rate and fulfillment | High discovery-to-purchase conversion |

| Merchant risk | Intermediary fees and ranking shifts | Platform dependency | Algorithm and trend dependency |

The Barrier to Dominance Is Distrust, Not Technology

While each company competes to become "the digital steward of consumer decision-making," the biggest obstacle is neither technology nor a rival but the shoppers' own distrust. As Schonthal puts it, platforms want to be more than where transactions occur — they want to be the steward of the decision. Yet shoppers are not ready to hand that steward the keys.

In research from Quad and The Harris Poll, 54% of Americans said they "find allowing AI access to their shopping history unappealing," and 73% said they feel "uneasy about how AI might use personal shopping data." Another 2026 survey found that 55% are now uncomfortable with AI agents completing purchases autonomously — a sign that the psychological hurdle tends to rise, not fall, as autonomy increases.

Which camp does this distrust favor? Horizontal agents, which hold sweeping cross-life data, are structurally more exposed as targets of privacy concern. Vertical players like Amazon, having already built trust confined to the shopping context, may face relatively less resistance to data use. The outcome of this power struggle is shifting from a question of feature superiority to one of how far shoppers are willing to delegate their trust.

For merchants, this bears directly on their own conduct, not just platform selection. As more transactions flow through AI agents, demands for transparency intensify — was a recommendation paid for, and how is the data handled? The design challenge is to keep distrust of a platform from being transferred onto your own brand.

What Merchants Should Be Designing Now

Concentrating optimization on a single platform is a dangerous bet in this contest. With no winner decided, the practical answer is to prepare across multiple touchpoints.

The top priority is structured product data that any agent can read. Mark up price, inventory, reviews, and shipping terms accurately, and your odds of being surfaced as a recommendation rise — on Google's UCP and on Amazon's assistant alike. Google's UCP is designed to interoperate with industry standards such as AP2, A2A, and MCP, so standards-aligned data preparation supports several camps at once.

Next, separate measurement and evaluation by traffic source. A referral from Gemini and a sale from TikTok Shop differ entirely in shopper intent and profit structure. Rather than lumping AI channels together, make ROI visible by camp using tools like GA4 custom channels to inform how you allocate limited resources.

Finally, keep auditing your dependence on the intermediary. What Alicia Gehring, VP of media strategy at WHITE64, worried about was exactly whether challenger brands can keep "attracting interested shoppers at a cost that makes sense." As long as Google controls intermediary fees and ranking priority, changes to those terms move your margins. Having your discovery entrance held by one company is the loss of negotiating power itself.

Conclusion

Google's Universal Cart was not merely a new feature but a declaration of intent to enclose the entire shopper journey. Yet that effort sits within a multipolar contest against camps with different strengths — Amazon's Alexa for Shopping, TikTok Shop, and Meta. The axis of competition is the fight between horizontal and vertical agents, and the final gate is consumer distrust. What merchants need is not to predict and bet on a winner but a design of distribution and transparency: structured data that gets picked up no matter which camp grows, measurement by camp, and vigilance against intermediary dependence.