Key Takeaways

- Alipay released an AI Open Platform for merchants, and combined with May's AI payment stack and June's AI-native app "Abao," Ant Group assembled the payment, entry, and supply layers of agent commerce in just three months

- Merchants register a service once as a plug-in, Skill, or agent, and it can then be invoked by any AI assistant across phones, cars, and smart terminals. It is an attempt to standardize agent-based discovery as a replacement for search advertising

- WeChat and JD.com are racing to build the same transaction layer in China. For e-commerce operators, the new question is how to design product data so an AI agent can find and transact it

The Transaction Layer for the Agent Economy Is Now Complete

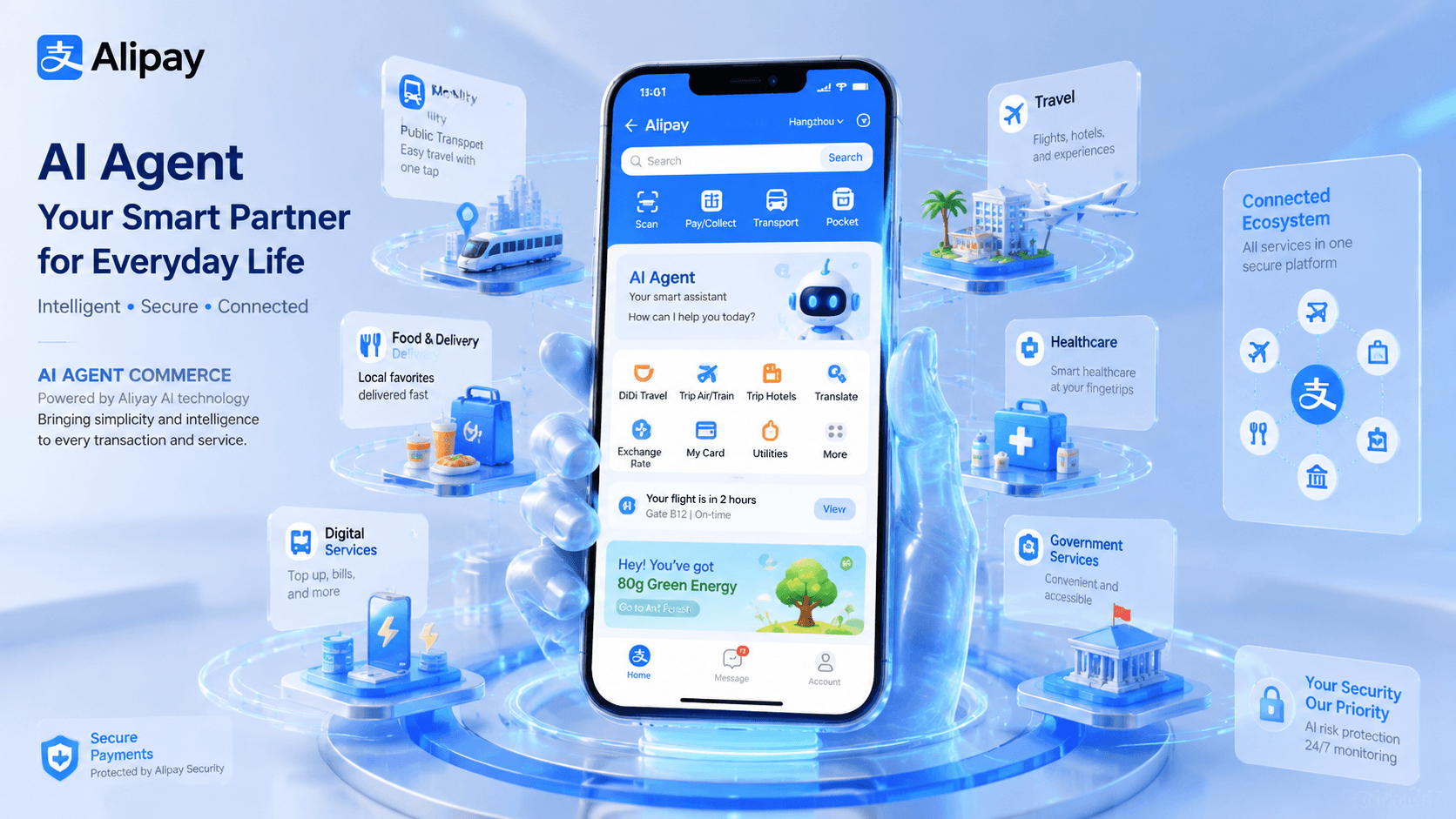

Alipay AI open platform lets merchants package services as plug-ins for AI agents across phones, cars, and terminals, completing Ant Group three-month AI commerce infrastructure buildout.

pandaily.comAlipay, China's payment giant operated by Ant Group, formally launched its AI Open Platform in July 2026. The platform lets merchants package their own services as plug-ins, Skills, or agents that can be invoked by AI assistants running across smartphones, in-vehicle systems, and other smart terminals, as reported by Pandaily.

The significance of this news is not a new feature. It is that Alipay has effectively completed the transaction layer for the emerging agent economy. Over a three-month sprint, the company shipped a full-stack AI payment product in May, the AI-native version of Alipay called "Abao" in June, and the merchant-supply platform in July. With payment, user entry, and merchant supply now in place, a complete loop exists for AI to discover and execute commerce.

Behind the move is a recognition that discovery itself is changing. Traditionally users typed keywords into a search box and compared options themselves. In agent commerce, a user tells an assistant what they want, and the assistant selects and executes the right service. Alipay is positioning itself as the hub for this new mode of discovery and transaction.

Connect Once, Reach Every AI Endpoint

The merchant value proposition is strikingly simple. Connect once to the platform and reach every AI endpoint, instead of building a separate integration for each AI assistant, smart terminal, or device ecosystem. From the user's side, a single natural-language request can retrieve, compare, and transact services across multiple providers without opening individual apps.

The first batch of connected merchants includes KFC, Mixue Bingcheng, Luckin Coffee, the mapping app Amap, and the ride-hailing platform Didi, covering food delivery, transportation, and lifestyle services that Chinese consumers use daily. Abao, already live, lets users invoke more than 10,000 everyday services through conversation, and the South China Morning Post called it the biggest Alipay overhaul in two decades.

Alipay president Li Jun described the platform as providing "a trusted, secure infrastructure for the future agent network interconnection." Rather than competing app by app, the intent is clearly to own the transaction foundation flowing underneath them.

Two Protocols Underpin the Trust Design

Once agents move money on a user's behalf, the central issue is trust and safety. Alipay's platform answers this with two foundational protocols.

The first is version 2.0 of ACT, the Agentic Commerce Trust Protocol, developed by the IIFAA internet trust alliance together with more than 20 partners including Zhipu AI. ACT first appeared in January 2026 as China's first open commercial technical protocol for agents. According to AIbase's explainer, it rests on four standards: a delegation-authority domain, a traceable operation chain, an intent-verification mechanism, and a secure payment channel. Crucially, every financial operation always requires explicit user authorization, with the AI acting as an executor rather than a decision-maker.

The second is the "Agent Hub Access" protocol for invoking services across devices and applications, standardized under the AI Agent Interconnect framework led by China's Ministry of Industry and Information Technology (MIIT). How AI discovers a merchant's exposed services and transacts them securely is being unified across the industry, in step with a government framework, which is a notable detail.

The scale claims have backing. Alipay disclosed that its AI payments processed 300 million cumulative agent transactions as of May 2026 and support 95% of general-purpose agent frameworks, per its announcement carried on businesswire. AI Pay had already crossed 100 million users in February, lending real substance to the claim of a commercially scaled AI-native payment rail.

China's Land Grab for the Transaction Layer

Reading Alipay's move as a single company's strategy would miss the point. In China, several giant platforms have started racing to own the agent transaction layer.

Symbolic of this is Alipay's calculated stance: the entry point is negotiable, but the payment core is not. According to 36Kr's analysis, WeChat holds roughly 70% of mini-programs while Alipay sits around 15%, putting Alipay at a disadvantage in the fight for the agent entry point. That is precisely why it anchors on the more fundamental, harder-to-replace payment layer, anticipating an era when users no longer consciously choose a payment tool because agents handle it.

Rivals have taken their positions too. WeChat, rather than rebuilding its payment app, is embedding payment capability inside agent products such as WorkBuddy and QClaw. JD.com released an autonomous-payment protocol called A2P2 in June, targeting the "last-mile trust problem" when agents transact without human oversight. UnionPay has shipped an AI payment product as well. Chinese consumers are unusually willing to delegate purchasing to AI: chinabizinsider notes about two-thirds are open to it, well above the roughly 40% global average, and that fertile ground is accelerating the race.

E-commerce Operators Must Design to Be Chosen by AI

Translated for e-commerce operators and marketers outside China, several concrete implications emerge.

First, the shift of discovery from search engines to AI agents is becoming irreversible, now cemented as infrastructure investment by a payment giant. Traffic once won through site SEO and ad spend gets replaced by a different logic in a world where agents pick products and services. Whether your product data, inventory, and pricing are published in a form an agent can read, compare, and act on becomes the new condition for shelf space.

Second, the hub model Alipay demonstrated, connect once and reach every endpoint, lowers integration cost for merchants while deepening dependence on the platform. Which protocol or foundation becomes the de facto standard will shape merchant bargaining power and fee structures. How far standards like ACT and Agent Hub Access spread is not someone else's problem.

Third, as Pandaily itself notes, it remains unproven whether agent-mediated discovery delivers returns comparable to advertising-based discovery. Whether merchants can recoup investment in agent channels is an open question, and the economics differ fundamentally from search and recommendation. Rather than treating connection to an agent as an end in itself, operators need to measure which channels actually generate transactions.

Conclusion

In three months, Alipay combined payment, entry, and supply into a standardized commercial infrastructure that other AI platforms can plug into, the most comprehensive attempt yet by a Chinese internet company to build the rails for agent commerce. The open questions of intent accuracy, handling failed transactions, and the economic model remain, but there is no doubt the mechanics of discovery and transaction are being quietly rewritten. What to watch next is how this hub-style standardization spreads beyond China, and when e-commerce operators elsewhere will have to face the AI agent as a new kind of customer.